Just over a year ago I wrote in the comments my prediction for 2012: "Prices will continue to creep down, and the 6 month average will end next year under $590k".

Well, that didn't quite pan out. Prices did nudge down, but the 6 month average as of Dec was $598k.

So I'll try again.

- VREB Sales for 2013: 5800

- 6 month SFH average in Dec 2013: $565,000

- BoC overnight rate Dec 2013: 1.0%

- Average MOI for 2013: 10

Monthly average and medians are far too volatile so I don't predict based on those. Over at VancouverCondoInfo they have a prediction contest for 2013 based on the MLS HPI for June and December. In little old Victoria we can use the Teranet index instead, so here's my prediction for Teranet values in 2013:

Teranet June 2013: 135

Teranet Dec 2013: 129

Anyone want to give theirs for the coming year?

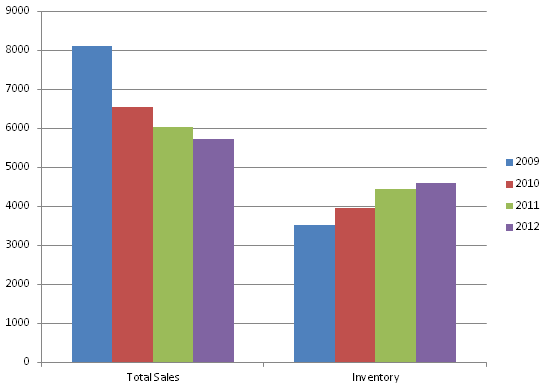

For context, here's a repost of some graphs showing current market conditions.

Teranet Dec 2013: 129

Anyone want to give theirs for the coming year?

For context, here's a repost of some graphs showing current market conditions.

|

|

|  |

|

|

247 comments:

«Oldest ‹Older 201 – 247 of 247Average prices do not work well at all. Toronto's housing market crashed in the early 90's and the official average price drop was something like 25%. However, there were many houses that were sold for 50-60% less than peak. This I know from talking to people who had to sell in that market and from talking with a long-time Toronto realtor.

Edmonton and Calgary were crashing very hard in 08-09. I followed the crashes in these cities closely and know that there were townhouses and condos that were selling for a full 50% below peak. Houses held their value a bit better, but some were selling for a third less than peak, even in nice areas. Again, officially, the average price dipped only 15-20% in these cities.

Info,

The market is not going to tank 50% no matter has many copy & paste jobs you do. Sorry.

Since Garth is 2 for 2 and batting 1.000 in the last 6 years when it comes to predicting housing busts in Canada, I will be posting regular excerpts from his blog.

Garth batting 1.0? Sorry, you just lost all credibility you never had.

Info, do me a favor. Watch this 4 year old video -> http://www.youtube.com/watch?v=1S7OumrfatY

Prices in Victoria are up since this video, ohhh, and interest rates haven't gone up as predicted by god Garth Turner, interesting, they've actually gone down. However, I know you will hail him as a hero when the BOC does eventually raise them .25% in the next two or three years.

He is also wrong about a multitude of other things.

I like Garth, smart guy, sells books, sells services, a really good writer but his followers for the most part can't think on their own for two minutes. Whatever he says they hail as correct and live in denial about Garth batting 100%

"Whatever he says they hail as correct and live in denial about Garth batting 100%"

As I wrote, Garth is 100% correct with his predictions about major Canada-wide housing market corrections over the last 6 years.

He predicted the current correction. As well, he predicted the crash of 08-09 which would have continued downward but it was halted by a massive, unprecedented, emergency intervention in early 2009. Nobody could have predicted that intervention, not even a realtor.

"The market is not going to tank 50% no matter has many copy & paste jobs you do. Sorry."

Where did I write that?

Which market? Victoria? Vancouver? Canada?

Barring a big enough intervention, we will see houses in Victoria metro selling for at least 50% below peak by the time this correction/crash is over.

"In June the Teranet was 140.4, in Nov it was 138.2 or a 1.6% decline. Nov 2011 it was 140.64, so YoY decline in the Teranet is 1.7%.

How is that a strong decline?"

I don't have the exact numbers, but it looks like the Teranet lost about 4 units in 4 months from July to the end of November. In comparison to the so called "stable" 6 month average, it is suggesting that a definite decline has started, maybe not a strong decline, yet.

The slope of the curve is the thing that is important here. Very steep. Annualized, that 4 units in 4 months would be 12 units in one year.

The Teranet numbers do not include December.

A drop of about 78 units would put us back at 2000 prices.

Watch this 4 year old video -> http://www.youtube.com/watch?v=1S7OumrfatY

Prices in Victoria are up since this video

Only because 4 years ago takes us to the trough of early 2009. Once we break through that - and it will happen - nominal prices will be the lowest since 2007.

Completely at odds with everything he is saying about a crash....and it's also idiotic.

It is actually exactly in line with what he is saying which is to diversify your investments.

Also it's not like this is his idea. This is the Smith Maneuver. Risky, but well known.

Get a secured HELOC for $200,000 . . . . and invest it in a balanced portfolio (my fav is 40% fixed, 60% growth) making 8% or so.

Ah yes - so housing is going to plummet hard, but the stock and bond markets will sail on merrily into the future without noticing the economic turmoil.

PS predicting future stock market returns based on past stock market returns is almost as smart as predicting future real estate trends by projecting past trends.

@info, and what followed the housing crash in the US?

As I wrote, Garth is 100% correct with his predictions about major Canada-wide housing market corrections over the last 6 years.

He predicted the current correction. As well, he predicted the crash of 08-09 which would have continued downward but it was halted by a massive, unprecedented, emergency intervention in early 2009. Nobody could have predicted that intervention, not even a realtor.

He is actually more wrong about Canada-wide than Victoria. For example, the Vancouver market is up over 30% since he started predicting a crash. If it drops 20% is he correct? No, anyone can predict a crash every month and eventually be right.

He also has predicted a TON of other things like the Olympics would hurt Vancouver and prices would come down, hmmm, they went up.

So if the market stays flat this year, what are you going to come with then? He couldn't have predicted how dumb buyers are? He is in the business of making predictions so there are no excuses "he couldn't have predicted that the government would lower interest rates in an economic downturn," seems fairly logical to me.

Must be joking.

How so? Do you mean to suggest that folks should just not own real estate, or that the stock market is about to crash, or what?

Turner's proposal otherwise seems to make perfectly good sense. If you own a house already, why pay off a 3% mortgage when the money you borrowed can earn 6%.

Barring a big enough intervention, we will see houses in Victoria metro selling for at least 50% below peak by the time this correction/crash is over.

Hope you are right. I'll be able to retire as we'll be able to buy a nice home in Oak Bay just off my girlfriend's public sector salary. If I decide to continue working maybe we'll look into waterfront.

Only because 4 years ago takes us to the trough of early 2009.

"Because" doesn't cut it for me, he was and still is wrong.

Developers are starting to see the writing on the wall.

http://www.cbc.ca/news/business/story/2013/01/10/business-building-permits.html

"Building permits are seen as a leading indicator of the economy because signal intentions to invest and build for the future, which people generally only undertake if they are feeling optimistic about the future."

Is Canada overbuilt? Not yet. Overbuilt implies that there is too much supply for the demand. Demand has been high because everybody and their dog have been buying every piece of property to get rental income, redevelop the land or just to hold. As housing slows this trend will also slow.

For all those years of overbuilding we will experience underbuilding because of a torrent of completions and people realizing they don't want to be amateur landlords.

Since our economy is so dependant on real estate, underbuilding necessarily means an increase in unemployment. Further, buying at the edge of your affordability is all the rage these days, expect to see a spike in the delinquency rates.

Or maybe that can't happen here...

How so? Do you mean to suggest that folks should just not own real estate, or that the stock market is about to crash, or what?

Turner's proposal otherwise seems to make perfectly good sense. If you own a house already, why pay off a 3% mortgage when the money you borrowed can earn 6%

He said 8%, not 6%.

I have about 35% equity in my condo and almost triple that invested in the stock market. I've also totally lucked out as I made large margin investments in 2009 and have returns of close to 100% on companies like BMO, 58% on TRP, 46% on RCI.B, etc., not including dividends. Also, totally lucked out maxing out my TSFA on a small growth company out of Vancouver as not only was the return big, I didn't have to pay tax on the gain :) and I'll do about 150 swing trades in my questrade account this year so I follow the market closely. So no, folks should not own just real estate.

However; for him to suggest borrowing money to invest into the TSX while predicting a housing crash, and quoting 8% return, is ridiculous in my opinion.

I can't see the housing market melting down across Canada and the TSX going up.

Also, if someone could successfully carry out 8% return for me year after year (after fees) I would sign up right away.

Reality is you could take out $200,000 at 3% and have a negative return of 20% in the first year, or worse. No big deal for someone in their 20s/30s, disasterous for someone in their 60s/70s which seems to be a lot of people calling into BNN to ask for advise.

This story on Reuters http://www.reuters.com/article/2013/01/10/us-usa-foreclosures-zombies-idUSBRE9090G920130110 about Zombie titles has many 'sub stories' within it that really highlight how dire things can get. Before jumping on our Canadian-high-horse the thing I think people should take from this is that the financial institution will win. They sell debt and reduce their own losses but the little person will not escape the debt. Note the story of the small business person (contractor) who went under because of the downturn in the housing market and lost both his business and his home. The other notable point is that upon death you do not avoid debt. These are heartbreaking and frightening stories. I hope we never see anything even close to this type of downturn.

Only because 4 years ago takes us to the trough of early 2009.

"Because" doesn't cut it for me, he was and still is wrong.

Only thing that matters for you or for me is how much you bought for and where prices move from then.

Do you think nominal prices will or will not drop below that trough in 2009? This is the predictions thread, let's have it.

@Leo, it's not the Smith Maneuver. Although that is not idiotic, it is extremely risky. Both involve leveraging your home into retirement wholly relying on YOUR investment portfolio returning 8%/year, timed perfectly to when you need it. The problem is you are pushing risk to later in life when you potentialy do not have the time or energy to weather a storm.

If you have ever invested, you will know the pain of money evaporating to nothing. You will know the truth that the mutual funds that returned 12% a year did so until it was sold to you, You will see that bewildering loss of 50% in a solid investment. The stock market is risky and on an individual stock basis, unpredictable... You should bankroll your investment portfolio in a similar way you would a poker bankroll. Start with what you can afford to lose and build it, increasing your bets as your bank roll grows. You don't leverage your home so you can start with a huge bankroll...

This is partly why I think the smith maneuver is not idiotic where what what Garth proposed is. In Garth's case the client owned their home free and clear. Giving them the ability to invest the money that would otherwise go to the mortgage into equities and other investments. Not fancy, but safer and you are not at the mercy of the bank if the sh*t hits the fan...

and since info didn't answer my question of what followed the housing crash in the states....answer is...the stock market crash of 2008-2009....

The fool who follows Garth Turner is the Greater Fool.

in Garth's case, using his assumptions, borrowing 200k will cost 1000/month to service (if you average a 4% rate for the next 25 years). Let's assume we can just whack 30% off that for tax purposes because we are investing outside an RRSP. So investing $700/month with that 8% return will give you 670k after 25 years. Plus you own your home out right, plus you had the flexibility to not pay if need be, plus you had the safety of not getting screwed by an interest rate spike....

He also predicted the crash of 08-09 that was, as we all know, halted by a dramatic, unprecedented, emergency intervention.

Look! It's info's favourite line: "unprecedented, emergency intervention."

This time, info used "dramatic" in front of it, but sometimes he uses "massive."

Let's start a drinking game based on info's repetition of this line.

... we're gonna get wasted!!!

228 comments. Time for a new thread?

1990 - Market Value of Publicly listed US Companies = 56% of US GDP

2012 Q3 - Market Value of Publicly listed US Companies = 125% of GDP

Hooray - let's use our (maybe) overvalued home to borrow money so we can put it in the (maybe)overvalued stock market.

Good advice Garth!

Germany really won WW2 except they were "halted by a dramatic, unprecedented, emergency intervention" by the Allies

@ Introvert

I'm flattered that you are starting to quote me.

@ dasmo

I've never said that a crashing housing market continues to crash until it hits a big fat zero. Currently, the US market, aided by considerable stimulus, including emergency interest rates, banks holding back massive amounts of shadow inventory and stacks of free cash for first time buyers, appears to possibly have hit bottom. Although some US economists are warning that it could also turn around again and hit new lows.

I wouldn't get too excited about the US housing market right now. What you should be getting out of their experience is the crash itself. They also believed it couldn't happen to them, which is the same attitude you and too many other Canadians currently have.

Their crash should be a lesson to all Canadians. Hundreds of thousands of US families still live with much financial hardship as a result of their housing bubble.

The Canadian housing market is in a more dangerous position than that of the US before it crashed.

* Canadian house prices are higher, on average, than the US peak

* Canadians currently have a higher debt/income ratio than what Americans had at market peak

* Overall, Canada's price/income ratio is higher than the US peak

* Canada's housing bubble peaked with emergency interest rates. The US, at least, had the ability to lower rates from 5-6% to 2-3% as a means of stimulus during their crash.

All of this while the two countries have similar incomes. We simply have less support for our bloated prices than the US had before their market crashed.

Introvert said:

The fool who follows Garth Turner is the Greater Fool.

IMO - only fools don't follow other's perspectives, on this blog as well as other blogs. Each blog has a style and using that lens when reading/scanning them is useful. Garth is a writer first and I get a lot of entertainment from the blog as well as learnings. In the year I've been following this blog I get more learnings but also some entertainment. I likely would have purchased in Victoria if it wasn't for this blog helping me become a better consumer and getting a more balanced perspective before I make a purchase (and I will because I do believe home ownership works for our family). My favourite part of blogs is the 'pile on' done to certain postings. I couldn't withstand the pressure like "info" does. I hope that these 'pile ons' don't shut down people sharing their interesting and helpful viewpoints. And I always appreciate Marko stepping forward in a transparent manner.

@Leo, it's not the Smith Maneuver

Functionally identical as far as I can see. Make the mortgage interest tax deductible by taking out equity in a LOC and investing it.

If you have ever invested, you will know the pain of money evaporating to nothing. You will know the truth that the mutual funds that returned 12% a year did so until it was sold to you, You will see that bewildering loss of 50% in a solid investment. The stock market is risky and on an individual stock basis, unpredictable.

So, very much like the housing market then. Except with stocks you generally don't leverage your investment 20 times. So when your ETF tanks by 20% you lose 20% of your money (on paper). When you put 5% down on a house and it declines by 20% you lose 400% of your money (nevermind transaction costs).

Let's assume we can just whack 30% off that for tax purposes because we are investing outside an RRSP. So investing $700/month with that 8% return will give you 670k after 25 years

I don't think you understand Garth's example. Investing the 200k minus interest on the HELOC gives you 1.16 million after 25 years. It's very risky, but it does make sense.

I wonder if Garth works for Investors Group, because that is something that they would try to pull. People should be happy beating term/GIC rates right now. Getting 8% is unlikely. Making money with your own cash is hard, making money with a 3% tail wind...

*head wind

"Functionally identical as far as I can see." Smith - you already have a mortgage. Garth - you owned the house free and clear. That's a big difference.

"So, very much like the housing market then." except you NEED a place to live and if it's paid for that's a huge necessity taken care of. Also removes a lot of financial risk moving forward...You don't need as much money. if your are not servicing debt.

"I don't think you understand Garth's example. Investing the 200k minus interest on the HELOC gives you 1.16 million after 25 years." I do get that..his suggestion makes perfect sense. As long as your portfolio performs at 8%/year for 25 years and rates stay around 4% for 25 years...

I suspect that the $10,000 incentive to buy a new home is kicking the crap out of the resale market for newer pre-owned houses in Sooke. And it isn't simply by an amount of $10,000. Because of the low sale volumes, prices for newer pre-owned homes are back into late 2005 or early 2006 levels. Making a home bought in say 2009 for $380,000 - now selling for under $300,000 today and that's for a six year old, 2000 square foot home in a new subdivision in Sooke.

That's a nutty crazy cheap price even for today's market. But, that's what happens when there is a "glut" of newer housing. It's also called an opportunity because of a nice re-bound effect once the glut is absorbed.

I know that most on this blogg don't really care about Sooke. Yet shallow markets, like the one we have today, present some good opportunities.

See, I'm not all doom and gloom. Those that have cash will have some fabulous buying opportunities over the next few years. Marko, might even be able to buy that waterfront home he wants. He'll just have to find another job, because there won't be any money in selling real estate.

Happy Camper thanks for the info once again. I am very familiar with on-line banking and transfers as I currently deal with 8 banks and credit unions using only the on-line banking method.

I have heard complaints from some whom have dealt with ICICI in the past...so I thought I would ask in here before I set up something with them.

Anyway I went in their website today and set up a High Interest Savings Account and TFSA GIC for five years at the 3.15%. I only buy GIC's for my TFSavings and purchase the max each year....this year the max amount is $5500. So now with the five years worth of savings I will be averaging 3.4%. Better than nothing for sure...and with virtually no risk.

"For all those years of overbuilding we will experience underbuilding because of a torrent of completions and people realizing they don't want to be amateur landlords.

Since our economy is so dependant on real estate, underbuilding necessarily means an increase in unemployment. Further, buying at the edge of your affordability is all the rage these days, expect to see a spike in the delinquency rates."

Scotiabank has also said that house prices in Canada will decline and stay down for a decade. They also expect a slowdown for the entire housing industry which will cause unemployment for the primary and related industries and have a negative impact on the entire economy.

I have to agree with them on that. Considering the source - a Canadian bank making a bearish prediction - it carries a lot of weight.

Let me add my predictions for December 2013.

In Oak Bay, we will see some house sales for at least 25% below peak price or peak assessment. We will see some condo/townhouse sales for at least 30% below peak.

The rest of my predictions will follow the same format.

In Saanich, Esquimalt, Langford, Metchosin and Colwood - 30% for houses and -35% for condos/townhouses.

Downtown - 25% for condos.

Sooke - 35% for houses.

"Another weak spot is the housing market, but the central bank’s analysis of slower sales and falling prices is more complex. Housing was the main engine of Canada’s escape from recession, but the cooling is mostly a relief – the central bank has deep concerns about the debt that Canadian households have piled up."

http://www.theglobeandmail.com/report-on-business/macklem-warns-canadas-outlook-weak-despite-recent-job-growth/article7191233/

The fool who follows Garth Turner is the Greater Fool.

If Turner had been hyping RE since 2008, he'd look more of a fool than Intro seems to think he is anyhow.

Turner correctly predicted the 2008 downturn but missed the government action to prop the market. That's because predictions are difficult, especially about the future. And that's why nobody ever gets all the money. The economic future is simply unknown.

But we still have to make investment decisions. Which is why, as Happy Camper states, its interesting to consider other people's ideas.

However; for him [Garth Turner] to suggest borrowing money to invest into the TSX while predicting a housing crash, and quoting 8% return, is ridiculous in my opinion.

He's not suggesting borrowing money to invest in the TSX. He's saying if you have 3% mortgage plus some cash, put the cash in the market, not necessarily the TSX, rather than pay down your mortgage.

For someone who boasts of investing on margin and making 100% annual return, your scathing comment about Turner's proposal seems rich.

If you follow Turner's advice and your stock nose-dives you've lost some of yer cash, but if you hang on for a few years you'll likely get it back unless you invested in something really daft.

If, on the other hand, you invest on margin and your stock nose-dives you're gonna be stopped out of the market for a big loss unless you can come up with more margin.

"Housing was the main engine of Canada’s escape from recession..."

The GFC started in late 2008. At this time, Canada was experiencing a serious, nation-wide housing correction that lasted into early 2009. Then the government slashed interest rates to emergency levels and brought in policy that allowed CMHC to insure even riskier mortgages. They expected this to turn the housing market around and it did. The other reason they did this was to allow an artificially stimulated housing market to artificially stimulate a fragile, weak economy. That also worked. At that time, the government began using the term "greenshoots" when referring to an improving economy. I laughed.

Canada didn't experience the economic hardships that the rest of the western world did over the last 4 years. A debt problem cannot be fixed (for the long term) with massive amounts of new debt, which is what was attempted in Canada. I think we will face the consequences of too much debt and then more and more debt, starting now. It will take years for this to play out, as it did in the US. They are still dealing with the consequences.

The US went through a lot of economic and financial hardship over the last 4 years. However, their future looks much brighter now. Houses cost a lot less and the average family can afford the average house. A lot of Americans have deleveraged and no longer have massive amounts of household debt weighing them down. Overall, the cost of living in the US is much lower than in Canada. As a result, some of the companies and businesses that left the US in recent years because it was too expensive to operate in there, have started to return. This is not happening in Canada, in fact, we are still seeing the opposite.

In the long run, a major housing correction will be better for the average Canadian family. We need to look past the here and now and consider future generations in Canada.

1990 - Market Value of Publicly listed US Companies = 56% of US GDP

2012 Q3 - Market Value of Publicly listed US Companies = 125% of GDP

Hooray - let's use our (maybe) overvalued home to borrow money so we can put it in the (maybe)overvalued stock market.

Profits per share for the S & P 500 rose 135% from 1990 to 2012, so the S & P was probably less overvalued last year than Victoria RE.

We need to ... consider future generations in Canada

Hey, where's your spirit of relentless greed. Future generations indeed. Soon you'll be proposing to overthrow the whole Liberal agenda of unrestrained hedonism, without the slightest thought for posterity.

Nanaimo killer deal of the week. $480k for a place that was listed originally for $789k and assessed @ $707k just this week....."

http://www.inmocentral.com/en/publications/59770-canada-british-columbia-290-woodhaven-drive-0#ad-image-5

Cheers,

The post gives an interesting insight into the Vancouver real estate. House hunting seems to be almost the same everywhere. A good study about the statistical information that is provided by the article about the real estate scenario.

Post a Comment