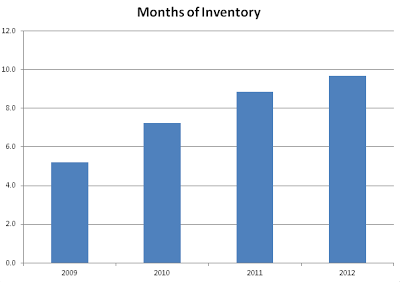

One of the best measures of current demand out there is the months of inventory (MOI). This expresses the number of months it would take to sell all active listings at the current monthly sales rate. So in September we had 419 sales with 5025 active listings, giving a MOI of 5025/419 = 12 months.

What does the MOI mean for prices? I'll let

this realtor from Phoenix explain:

It’s widely agreed that when inventory levels fall between 5 & 7 months, that the market will be considered balanced. Housing prices should be stable, perhaps rising slightly, influenced more by inflation than by demand. When inventory levels exceed 7 months, then the demand for housing is low, and prices are likely to fall. The high number of homes for sale will create a buyer’s market, allowing buyer’s to dictate price and terms to the majority of sellers if a seller wants to make a deal. When inventory levels fall below 5 months, sellers have more control over price and terms, often resulting in a more significant rise in housing prices, aka a seller’s market.

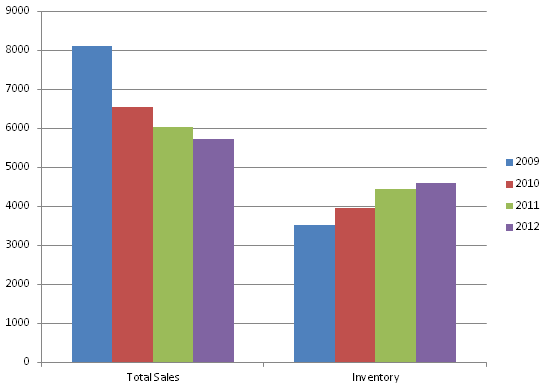

So let's take a look at the last 7 years in Victoria history. Note that months of inventory is for all

residential properties in greater Victoria, including single family homes, condominiums, townhouses, and manufactured homes. Previously I only had monthly data back to mid 2008, but

Marko Juras has kindly provided monthly price, new listings, and sales data going back to 1990. Huge thanks for that!

|

| Victoria Residential MOI and SFH Price (click to enlarge) |

Another way to look at the same data is by time. Clearly during the boom times we were in a sellers market with months of inventory going as low as 2 and prices increasing by double digits. HouseHuntVictoria was founded just as Victoria's market first briefly strayed into balanced territory (Feb 2007, not marked as green) however the boom wasn't done yet, and went on for another year. Fall of 2008 brought the financial crisis and MOI went through the roof causing prices to drop steeply. However the government crashed interest rates and let loose the lending taps to bring the market back to sellers and prices to recover. Since 2010 we've been in a buyers market with a gentle decline in prices.

What will happen next? It's anyone's guess but notice the steep rise in MOI in the past few months. We are now at the highest level since the financial crisis. Of course the fall will bring some declines here, so another way to look at it is by factoring out seasonal variations and examining the 12 month rolling average of both price and MOI.

Next up: What does a market bottom look like? Can it be predicted by the MOI?

UPDATE: How odd is 12 months of inventory in September? Very odd.